The spring housing market has gotten off to a sluggish start due to higher mortgage rates, but new-home sales appear to be a bright spot.Sales of newly built single-family homes jumped nearly 9% in March, reaching their highest level since last fall, the Commerce Department reported Tuesday. With limited inventory options in the resale market, more buyers are eyeing new construction.Home builders are showing more willingness to offer incentives,

More Americans than ever are priced out of the housing market and President Biden has outlined steps his administration is taking to increase development of affordable housing.In the 2024 Economic Report of the President, President Biden said housing shortages and unaffordability have risen dramatically over the past 60 years, primarily affecting low- and middle-income families. The President mostly blames the nation’s affordable housing s

Economists have been scratching their heads over how Americans can continue to prop up the economy with their spending despite high interest rates, persistent inflation, dwindling savings and rising debt.There may be a simple answer: Jobs.Payroll growth has been stunningly strong this year. Most people who land new jobs have been opening their wallets, with many making big lifestyle changes that include buying a new house or car, according

Home buyers are left pondering: Lock in now or wait and see?Mortgage rates surged this week, jolting home buyers who may have just started to grow accustomed to borrowing costs in the 6% range. The 30-year fixed-rate mortgage rose to a 7.1% average this week, its highest level since last December, Freddie Mac reports.“As rates trend higher, potential home buyers are deciding whether to buy before rates rise even more or hold off in hopes of dec

The smart lock landscape in 2024 showcases an array of options tailored to enhance security and convenience in modern homes.Smart locks continue to redefine home security and convenience in 2024. The innovation of smart locks is evident with enhanced connectivity, security features and seamless integration with smart home systems. Having personally tested over 30 smart locks, I’ve put together a list of my top recommendations, trends and featur

Higher-than-expected inflation data is expected to push borrowing costs up during the busy homebuying season.Mortgage rates are inching toward 7% after new data this week revealed a sensitive economy still coping with stubbornly high inflation. The 30-year fixed-rate mortgage now averages 6.88%, Freddie Mac reports.“If one were to shake a Magic 8 Ball, the answer to the question of ‘where are mortgage interest rates going to be in the next mo

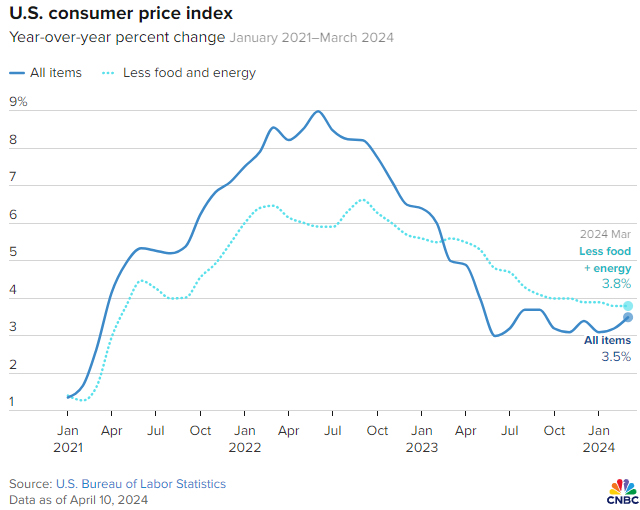

The consumer price index accelerated at a faster-than-expected pace in March, pushing inflation higher and likely dashing hopes that the Federal Reserve will be able to cut interest rates anytime soon.The CPI, a broad measure of goods and services costs across the economy, rose 0.4% for the month, putting the 12-month inflation rate at 3.5%, or 0.3 percentage point higher than in February, the Labor De

Bond market investors who fund most mortgage loans are increasingly convinced the latest inflation numbers mean the Federal Reserve won't cut rates in June With would-be homebuyers already in retreat, mortgage rates soared to new 2024 highs Wednesday after yet another discouraging inflation report pushed the prospect of Federal Reserve interest rate cuts further into the future.Applications for purchase loans were down by a seasonally adjusted 5

United States property investors are putting the pedal to the metal and feeling optimistic despite a turbulent housing market United States property investors are putting the pedal to the metal and feeling optimistic despite a turbulent housing market, according to a pair of reports.The share of homes purchased by investors reached a new high in the fourth quarter of 2023, and investor sentiment remains relatively high heading into the

U.S. prices moderated in February, with the cost of services outside housing and energy slowing significantly, keeping a June interest rate cut from the Federal Reserve on the table.The report from the Commerce Department on Friday also showed consumer spending rising by the most in just over a year last month, underscoring the economy's resilience. The United States continues to outperform its global peers despite higher borrowing costs, thanks

Stay up to date on the latest real estate trends, valuable tips, and company news.

This website includes images sourced from third party websites including Adobe, Getty Images, and as otherwise noted.