The smart lock landscape in 2024 showcases an array of options tailored to enhance security and convenience in modern homes.Smart locks continue to redefine home security and convenience in 2024. The innovation of smart locks is evident with enhanced connectivity, security features and seamless integration with smart home systems. Having personally tested over 30 smart locks, I’ve put together a list of my top recommendations, trends and featur

Higher-than-expected inflation data is expected to push borrowing costs up during the busy homebuying season.Mortgage rates are inching toward 7% after new data this week revealed a sensitive economy still coping with stubbornly high inflation. The 30-year fixed-rate mortgage now averages 6.88%, Freddie Mac reports.“If one were to shake a Magic 8 Ball, the answer to the question of ‘where are mortgage interest rates going to be in the next mo

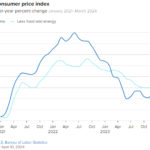

The consumer price index accelerated at a faster-than-expected pace in March, pushing inflation higher and likely dashing hopes that the Federal Reserve will be able to cut interest rates anytime soon.The CPI, a broad measure of goods and services costs across the economy, rose 0.4% for the month, putting the 12-month inflation rate at 3.5%, or 0.3 percentage point higher than in February, the Labor De

Bond market investors who fund most mortgage loans are increasingly convinced the latest inflation numbers mean the Federal Reserve won't cut rates in June With would-be homebuyers already in retreat, mortgage rates soared to new 2024 highs Wednesday after yet another discouraging inflation report pushed the prospect of Federal Reserve interest rate cuts further into the future.Applications for purchase loans were down by a seasonally adjusted 5

United States property investors are putting the pedal to the metal and feeling optimistic despite a turbulent housing market United States property investors are putting the pedal to the metal and feeling optimistic despite a turbulent housing market, according to a pair of reports.The share of homes purchased by investors reached a new high in the fourth quarter of 2023, and investor sentiment remains relatively high heading into the

U.S. prices moderated in February, with the cost of services outside housing and energy slowing significantly, keeping a June interest rate cut from the Federal Reserve on the table.The report from the Commerce Department on Friday also showed consumer spending rising by the most in just over a year last month, underscoring the economy's resilience. The United States continues to outperform its global peers despite higher borrowing costs, thanks

iPro was founded on the idea of building a better living with champion real estate services. We focus on incorporating and mastering the latest technologies and perform all types of real estate transactions. Our team of professionals set a stronger standard of business and give superior results.REALTORS: Enjoy a suite of benefits including free leads, low fees, 24/7 broker support, a complimentary agent website, drip marketing tools, and the free

Mortgage rates moved down a bit this week, in line with the benchmark 10-year Treasury, as the markets continue to digest comments from Federal Reserve members.The 30-year fixed loan averaged 6.79% as of Thursday morning, down 8 basis points from the previous week's 6.87%, according to the Freddie Mac Primary Mortgage Market Survey. For the same period last year, the average was 6.32%.Meanwhile the 15-year FRM averaged 6.11%, down from

We've upgraded our website with a newly advanced AI-induced listing search engine along with additional features throughout the website that offer a more captivating experience. The new search capabilities include an inviting process that accepts more usual search engine lingo and can be activated with standard search prompts. For example, you can search: "Looking for a 4 bedroom 3 bath house within 30 miles of Los Angeles for $2-5 million with a

From our home to yours... We hope you have a fun and lovely Easter Sunday.

Stay up to date on the latest real estate trends, valuable tips, and company news.

This website includes images sourced from third party websites including Adobe, Getty Images, and as otherwise noted.